Are you looking to protect your most valuable investment? Homeowners insurance is a crucial aspect of safeguarding your home and belongings. Understanding how homeowners insurance rates are calculated can help you make informed decisions about coverage options. In this blog post, we will explore the factors that influence homeowners insurance rates, compare rates across different states, provide tips for lowering premiums, analyze various policies, and emphasize the importance of regularly reviewing your coverage. Let’s dive into the world of homeowners insurance rates comparison to ensure you have the best protection at the right price!

Understanding Homeowners Insurance Rates

Homeowners insurance rates are determined by a variety of factors that assess the risk associated with insuring your home. Insurers consider aspects such as the location of your property, its age, construction materials, and proximity to potential hazards like flood zones or wildfire-prone areas. Your home’s replacement cost also plays a significant role in calculating insurance premiums, as more expensive homes typically require higher coverage limits.

Additionally, personal factors like your credit score, claims history, and the presence of safety features in your home can influence the rate you are quoted for homeowners insurance. Understanding these elements can help you comprehend why certain policies may be priced higher or lower than others.

It’s essential to grasp how insurers evaluate these variables to make informed decisions when selecting a homeowners insurance policy that meets your needs while staying within budget.

Factors That Affect Homeowners Insurance Rates

When it comes to homeowners insurance rates, there are various factors that can impact how much you pay for coverage. One significant factor is the location of your home. Homes in areas prone to natural disasters like hurricanes or earthquakes may have higher insurance rates due to the increased risk of damage.

The age and condition of your home also play a role in determining your insurance premiums. Older homes or properties with outdated plumbing, electrical systems, or roofing may be more expensive to insure as they pose a higher risk for potential claims.

Your credit score can also influence your homeowners insurance rates. Insurers often use credit-based insurance scores to assess the likelihood of you filing a claim. A lower credit score could result in higher premiums.

Additionally, the coverage options you choose and the amount of coverage you need will affect your homeowners insurance rates. Opting for add-ons like flood insurance or a lower deductible will increase your premiums, while choosing basic coverage limits may help keep costs down.

Other factors that can impact your homeowners insurance rates include the size and construction materials of your home, as well as any previous claims history on the property. Understanding these factors can help you make informed decisions when shopping for homeowners insurance policies.

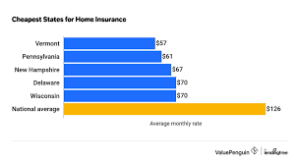

Top 5 States with the Highest and Lowest Homeowners Insurance Rates

When it comes to homeowners insurance rates, the state you reside in plays a significant role. Let’s take a look at the top 5 states with the highest and lowest homeowners insurance rates in the United States.

Starting with the states that have some of the highest premiums, Florida tops the list due to its exposure to hurricanes and severe weather conditions. Louisiana follows closely behind, also facing high risks of natural disasters like hurricanes and flooding.

On the other end of the spectrum, states like Idaho and Oregon typically have lower homeowners insurance rates. These regions experience fewer extreme weather events compared to coastal areas, resulting in more affordable premiums for homeowners.

Texas falls somewhere in between – while parts of Texas face high insurance costs due to their vulnerability to hurricanes and tornadoes, other areas enjoy relatively lower rates.

Understanding how your state’s risk factors impact your homeowners insurance rates can help you make informed decisions when choosing coverage options.

Tips for Lowering Your Homeowners Insurance Rates

Looking to save some money on your homeowners insurance rates? Here are some tips that can help you lower your premiums:

1. Increase Your Deductible: Opting for a higher deductible can lower your monthly premium, just make sure you have enough set aside in case of a claim.

2. Bundle Your Policies: Most insurance companies offer discounts if you bundle your homeowners and auto policies together with them.

3. Improve Home Security: Installing security features like alarm systems or deadbolts can reduce the risk of theft or damage, potentially lowering your rates.

4. Maintain Good Credit: Many insurers take credit scores into account when determining rates, so keeping good credit can work in your favor.

5. Shop Around: Don’t settle for the first quote you receive! Compare different insurers to find the best rate that fits your needs and budget.

Comparison of Different Homeowners Insurance Policies

When it comes to homeowners insurance policies, there are various options available in the market. It’s essential to compare different policies to find one that suits your needs and budget.

Each policy may offer varying coverage limits, deductibles, and additional features like personal property protection or liability coverage. Some policies may also include extras such as identity theft protection or equipment breakdown coverage.

Comparing policies can help you determine which ones provide the best value for your specific requirements. Be sure to look at not just the premium cost but also the extent of coverage offered by each policy.

Reading through the fine print is crucial when comparing policies, as terms and conditions can vary between providers. Pay attention to any exclusions or limitations that may impact your decision-making process.

Taking the time to compare different homeowners insurance policies ensures that you make an informed choice that protects your home and belongings adequately.

Importance of Regularly Reviewing and Updating Your Policy

Regularly reviewing and updating your homeowners insurance policy is crucial to ensure that you have adequate coverage for your home. Life changes, and so do your insurance needs. By taking the time to review your policy annually or whenever there are significant changes in your life or home, you can avoid gaps in coverage or paying for unnecessary extras.

Make it a habit to check if the value of your home has increased due to renovations or market fluctuations. This will help you adjust the dwelling coverage limit accordingly. Additionally, consider any new valuable items you may have acquired that would require additional personal property coverage.

Stay informed about any updates in local building costs and regulations that could affect the cost of rebuilding your home in case of damage. Reviewing these factors with your insurance provider can ensure you are adequately protected against unforeseen events.

Remember that proactive maintenance, such as installing security systems or upgrading plumbing/electrical systems, could potentially lower premiums. Keeping an open line of communication with your insurer allows for adjustments that reflect these improvements while keeping costs down.

Don’t wait until disaster strikes to realize gaps in coverage – stay ahead by regularly reviewing and updating your homeowners insurance policy!

Final Thoughts and Recommendations

Final Thoughts and Recommendations

As a homeowner, it is crucial to understand the factors that influence your insurance rates. By being aware of these variables and taking steps to mitigate risks, you can potentially lower your homeowners insurance premiums. Remember, each state has its unique considerations when it comes to insurance rates, so comparing quotes from different providers is essential.

Regularly reviewing and updating your policy is also key. Life changes such as renovations or additions to your home, acquiring valuable items, or even just the passage of time can impact your coverage needs. Stay proactive in managing your policy to ensure you have adequate protection for your home and belongings.

In the end, finding the right balance between coverage and cost is paramount. While saving money on premiums is important, it should not come at the expense of insufficient coverage when you need it most. Take the time to research different policies, compare rates, and consult with an insurance agent if needed to make informed decisions about protecting one of your most significant investments – your home.

We hope this guide has provided valuable insights into understanding homeowners insurance rates comparison and how you can make informed choices to secure a reliable policy that fits both your budget and protection needs. Stay vigilant in monitoring changes in market trends and policy offerings to ensure you are always getting the best value for your homeowners insurance coverage.